Statute of Limitations by State For Commercial Collections

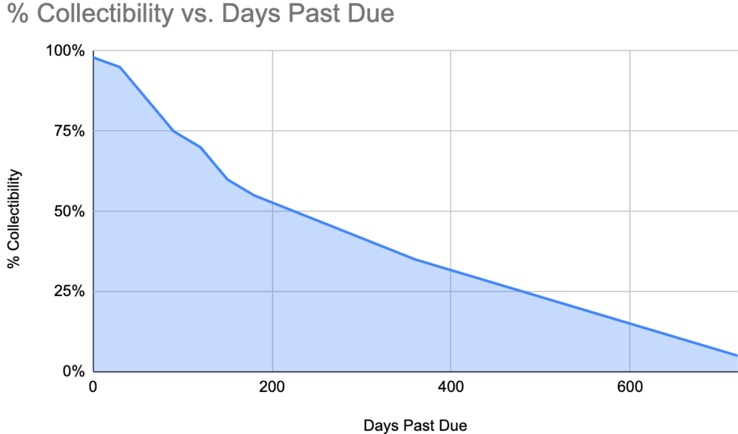

The Statute of Limitations for lawsuits varies by state, and runs anywhere from 3 to 15 years, after which the debt is “time-barred,” and you cannot sue.

You should use every legal means at your disposal, of course, but if you wait too long and rely on a last-minute lawsuit as a hail-mary effort to collect what is due, you may be very disappointed. Time is not on your side.

Inevitably, the action will be stretched out, and litigation will be very expensive. The older the debt, the more convinced a debtor is that they will never have to pay, at least the full amount, and the more the claim will be subject to made-up disputes, and you will have great difficulty finding witnesses to testify.

And, of course, the present value of a possible recovery years later if you prevail in court and the debtor is still in business when you get a judgment is much less than the amount owed.

- Never let your receivables age to the point you are concerned about the Statute of Limitations.

- We recommend you use your commercial collection agency to negotiate the best deal they can, and then move on to new business.

Below is a rough guide only, and not legal advice. You will need to know when the statute of limitations begins to run, and the events that may occur that will delay it. The list below is indicative only but should be of some guidance to you; it does not cover government, injuries or property damage. Always check the current state statutes to be sure, and here is a link to a site with more detail if you need to do some research.

| Contracts | Contracts | ||||

| State | Written | Oral | State | Written | Oral |

| Alabama | 6 | 6 | Montana | 8 | 5 |

| Alaska | 3 | 3 | Nebraska | 5 | 4 |

| Arizona | 6 | 3 | Nevada | 6 | 4 |

| Arkansas | 5 | 3 | New Hampshire | 3 | 3 |

| California | 4 | 2 | New Jersey | 6 | 6 |

| Colorado | varies | varies | New Mexico | 6 | 4 |

| Connecticut | 6 | 3 | New York | 6 | 6 |

| Delaware | 3 | 3 | North Carolina | 3 | 3 |

| DC | 3 | 3 | North Dakota | 6 | 6 |

| Florida | 5 | 4 | Ohio | 8 | 6 |

| Georgia | 6 | 4 | Oklahoma | 5 | 3 |

| Hawaii | 6 | 6 | Oregon | 6 | 6 |

| Idaho | 5 | 4 | Pennsylvania | 4 | 4 |

| Illinois | 10 | 5 | Rhode Island | 10 | 10 |

| Indiana | 10 | 6 | South Carolina | 3 | 3 |

| Iowa | 10 | 5 | South Dakota | 6 | 6 |

| Kansas | 5 | 3 | Tennessee | 6 | 6 |

| Kentucky | 10 | 5 | Texas | 4 | 4 |

| Louisiana | 10 | 10 | Utah | 6 | 4 |

| Maine | 6 | 6 | Vermont | 6 | 6 |

| Maryland | 3 | 3 | Virginia | 5 | 3 |

| Massachusetts | 6 | 6 | Washington | 6 | 3 |

| Michigan | 6 | 6 | West Virginia | 10 | 5 |

| Minnesota | 6 | 6 | Wisconsin | 6 | 6 |

| Mississippi | 6 | 3 | Wyoming | 10 | 8 |

| Missouri | 10 | 5 | |||

If you have aged accounts, call us for advice, or start to start debt collection on your behalf.