Accounts Receivable deductions can dilute revenues from 5% in industrial companies to 20% in consumer products companies. These deductions arise from various issues, including ordering and billing errors, returned merchandise, pricing discrepancies, trade promotion deals, payment discounts, shipping errors, and non-compliance with customer vendor policies.

Deduction overcharges, far from being exceptional, are a common occurrence. Many deductions contain errors that can significantly impact sellers’ profits. For instance, up to 50% of returns are overstated due to SKU, price, or quantity errors. Post-audit deductions, which result from post-payment reviews, can be over 75% incorrect. Errors in trade deals and volume discount deductions are often substantial. These inaccuracies underscore the need for efficient reconciliation and resolution processes to mitigate the potential for significant and sometimes hidden revenue and profit losses.

Reconciling deductions against related credit memos is challenging due to the volume and variety of SKUs. Our extensive experience and specialized software enable us to reconcile and identify overcharges on any scale, even spanning several years for a trading partner.

Deduction Staff and Systems

Other crucial factors in managing deductions include the experience of your staff and the time available to pursue these claims. The most effective A/R systems utilize automated bots to access claims from major retailers before deductions are made, allowing more time to resolve issues before automatic deductions occur. Some chain retailers even have time periods, say 60 days, after which they consider their claim valid and won’t discuss it. This underscores the need for a strategic approach to deduction management, considering both your staff’s capabilities and the process’s time constraints.

Twenty years ago, many deductions were “negotiable,” and 50/50 across-the-board settlements were sometimes possible. Today, you must prove the customer is wrong in specific detail and do it quickly. While most deductions are generally accurate, the average recoverability on gross deducted amounts ranges between 10% and 20%, depending on factors like your industry, customer base, processes, systems, and the speed of your investigation. There is a lot of money involved.

Information You Get from Analyzing Deductions

Analyzing customer Accounts Receivable (A/R) deductions can uncover various operational errors impacting a company’s financials and operations, so your systems should include root cause accountability, enabling you to eliminate systemic process failures. Here are some common types of operational errors that can be identified:

1. Pricing Errors

- Incorrect Pricing: Not billing according to the P.O. terms.

- Misapplied Discounts: Applying discounts incorrectly or not applying agreed-upon discounts.

- Price Changes Not Updated: Customer failure to update systems with current pricing information.

2. Shipping and Delivery Errors

- Incorrect Shipments: Using the wrong carrier, not calling for appointment windows.

- Late Deliveries: Delivering products later than agreed, causing penalties.

- Shipping Damage: Products damaged during shipping, leading to returns or deductions.

- Freight Charges Errors: Incorrectly billed shipping and handling charges.

3. Compliance and Contractual Errors

- Non-Compliance with Vendor Policies: Not adhering to customer’s specific vendor compliance requirements.

- OTIF failures

- Contractual Non-Compliance: Failing to meet terms and conditions stipulated in contracts.

- EDI Errors: Issues related to Electronic Data Interchange, such as incorrect formats or missing data.

4. Trade Promotion and Discount Errors

- Promotion Misapplication: Incorrectly applying trade promotions and discounts.

- Unauthorized Deductions: Customers taking unauthorized deductions without proper agreement.

- Rebate and Allowance Mismanagement: Errors in calculating or applying rebates and allowances.

5. Returns and Refund Errors

- Misprocessed Returns: Incorrect processing of returned goods, leading to overstated returns.

- Return Authorization Issues: Not properly authorizing returns, resulting in disputes and deductions.

- Restocking Fee Misapplication: Failing to apply restocking fees where applicable.

6. Order Processing Errors

- Order Entry Mistakes: Errors in entering orders into the system, leading to incorrect fulfillment.

- Miscommunication: Issues stemming from poor communication between sales, billing, and shipping departments.

7. Inventory and Stock Management Errors

- Stock-Out Situations: Failure to fulfill orders due to inventory shortages.

- Overstock Situations: Accumulating excess inventory leading to potential obsolescence or markdowns.

- Incorrect Stock Levels: Discrepancies between actual and system-recorded inventory levels.

8. Data Entry and System Errors

- Manual Entry Errors: Mistakes in entering data manually, leading to inaccuracies.

- System Integration Failures: Problems with the integration between different systems, causing data inconsistencies.

- Outdated Information: Using outdated customer or product information in transactions.

By identifying and addressing these operational errors through A/R deductions analysis, companies can improve their processes, reduce revenue leakage, and enhance overall operational efficiency.

Lastly — Time is of the Essence to Recovery of Deduction Errors

The collectibility of deductions varies based on the type of claim, the systems and documentation you have, and the time it takes to complete your investigation and reconciliation.

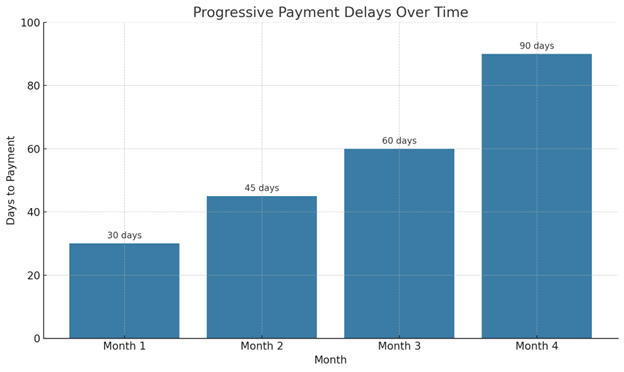

A critical factor is the time it takes to research, reconcile, and prove overcharges, which often takes months, during which the likelihood of collectibility plummets. Deduction value depreciates far faster than invoice receivables so time is of the essence in tackling this challenge.

For instance, while an average overcharge rate of 14% might be assumed, this figure can be misleading. Some deductions may be entirely uncollectible (0%), while some may be fully recoverable (100%). The true nature of each deduction is only revealed through a thorough investigation.

This is where the value of intelligent automation and experienced deduction audit staff becomes evident. Automated A/R systems, like Smyyth’s advanced Carixa, for example, can cut the time it takes to document deductions from weeks to one or two days, immensely increasing the collection rate of deduction errors. Professional staff with access to this type of software could produce ROI of 100% or more.

From the practitioners at Smyyth LLC